Two weeks into a market downturn and the questions are getting harder. Bitcoin is trading below USD$61,000 (AU$86,906.94), gold fell with it, and a US inflation print is sitting on the calendar like a threat. Meanwhile a Reuters investigation put numbers to something the industry has long suspected about Trump's crypto ventures, SBF filed for a pardon with a straight face, and Anthropic's most advanced AI briefly sent DeFi Twitter into a spiral. Underneath all of it, some serious voices are still making the case that the next version of this industry looks nothing like the one currently selling off. Let's get into it.

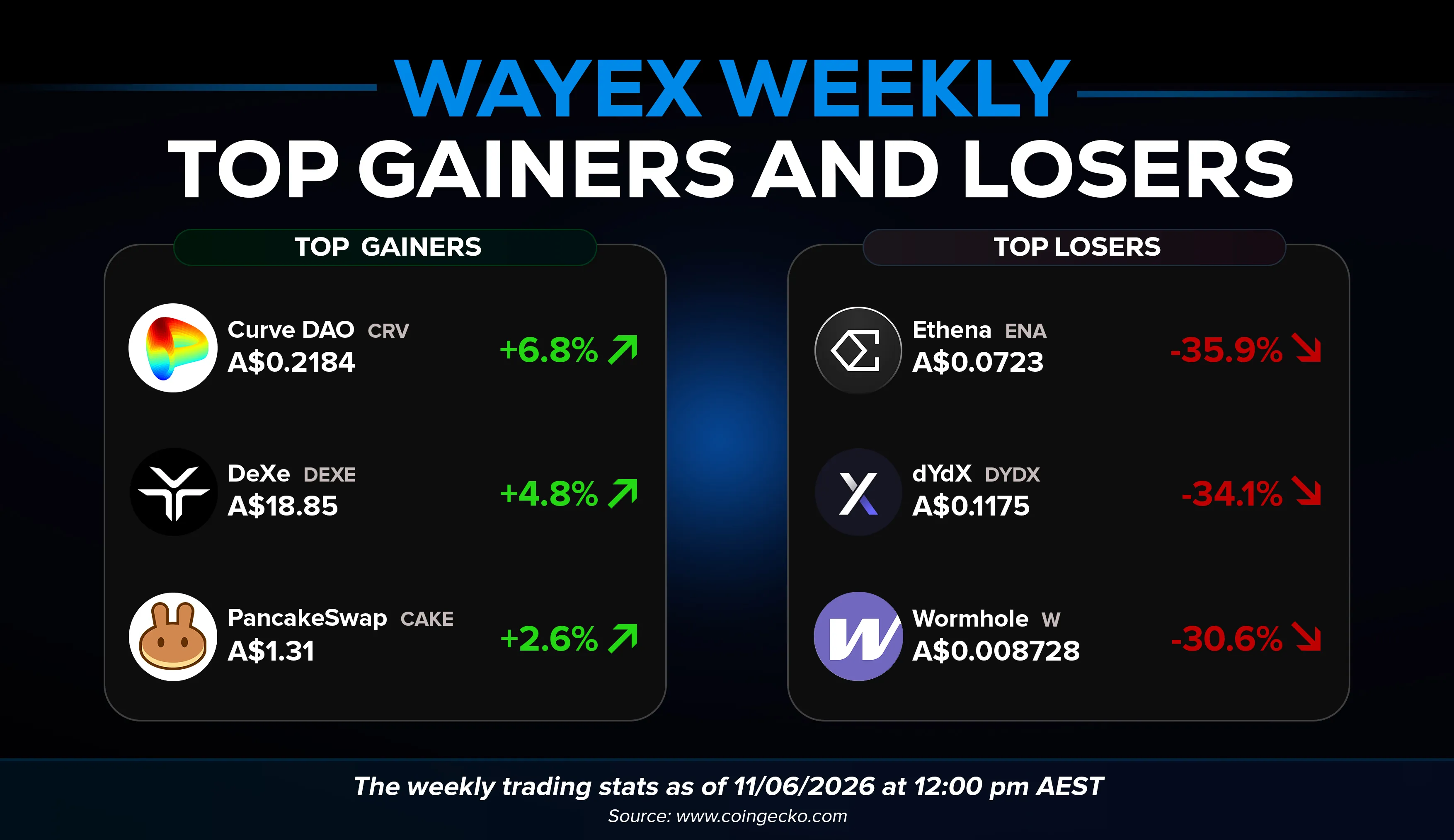

Top Gainers & Losers on Wayex

The Bounce That Fooled Nobody

Bitcoin's brief recovery from last week's lows did not last. BTC fell back below USD$61,000 (AU$86,906.94) this week, down nearly 7% on the week, while gold slipped below USD$4,200 (AU$5,983.76) an ounce in the same session. The two assets rarely fall in lockstep. Both are stores of value that pay no yield, which means both lose their appeal when traders start betting on higher interest rates, and that is exactly what is happening. Markets are now bracing for a US inflation print that could harden the case for Federal Reserve Chair Kevin Warsh to keep rates elevated for longer. A hot reading would drain liquidity from the assets that ran hardest on cheap money, and Bitcoin is near the top of that list.

The bounce that ran into Monday turned out to be a short squeeze rather than fresh buying. More than USD$500 million (AU$712.35 million) in bearish bets were liquidated, the highest such figure since April, but spot demand never showed up behind it. US Bitcoin ETF outflows have kept institutional money cautious, and as Diana Pires, chief business officer at sFOX, put it, when new demand is not broad enough to cover the selling, rallies struggle to hold. Ethereum fell 3.4% to around USD$1,625 (AU$2,315.14), Solana dropped 4.1%, and XRP lost 4.3% in the same period.

The question the inflation print raises is one the market has been avoiding for weeks. If gold steadies and Bitcoin keeps falling when rates stay high, the case for Bitcoin as a macro hedge weakens in the short term. The longer-term structural argument that Bitcoin outperforms on a liquidity-adjusted basis over meaningful time horizons has not changed. What changes week to week is how much patience that argument requires. Right now it is requiring quite a lot.

Trump Family Won. Investors Didn't

A Reuters investigation published this week put hard numbers on something the industry has long suspected. The Trump family has extracted an estimated USD$2.3 billion (AU$3.28 billion) from their main crypto ventures since returning to the White House, while investors in those same products recorded losses of roughly the same amount. The review covered four businesses: World Liberty Financial, the $TRUMP meme coin, AI Financial Corp (formerly Alt5 Sigma), and American Bitcoin. The pattern across all four was consistent. The family risked little of its own capital while earning revenue through token sales, licensing arrangements, equity-linked structures, and promotional activity. Investors bought in when excitement was high and absorbed the losses when prices fell.

The Alt5 Sigma story needs to be addressed. The company raised USD$750 million (AU$1.07 billion) from investors and used most of the proceeds to buy World Liberty Financial tokens directly from the Trump family's venture at a premium price. More than USD$500 million (AU$712.35million) from that transaction flowed to Trump entities. Alt5's share price has since fallen more than 90% from its peak, and the company, now rebranded as AI Financial Corp, has warned investors about its ability to continue as a going concern. Ethics watchdogs and former regulators have called on the SEC to investigate the company's disclosures and the conflicts of interest arising from its relationship with the president's family. The White House has maintained that there are no conflicts of interest.

None of this is straightforward to write about, and we want to be clear about what it is and what it is not. It is a documented, sourced account of who made money and who lost it in a series of crypto ventures connected to the sitting US president. It is not a reason to dismiss the broader regulatory progress happening in Washington, which remains real and consequential for Australian crypto users. What it is a reason to do is apply the same scepticism to politically connected crypto projects that you would apply to any other investment. The conflict of interest is not a theory. The numbers are public record.

SBF Wants a Pardon. Trump Said No

Sam Bankman-Fried, the founder of the collapsed crypto exchange FTX, formally filed for a presidential pardon this week while serving a 25-year sentence for fraud and conspiracy. The application appeared in records maintained by the US Department of Justice's Office of the Pardon Attorney, listed as pending. The request is specifically for a pardon after completion of sentence, meaning Bankman-Fried is not asking to walk free immediately. However, he is simultaneously pursuing an appeal of his conviction in federal court in New York.

The filing is a long shot by almost any measure. Trump told the New York Times in January that he has no intention of pardoning Bankman-Fried, grouping him alongside other figures he described as undeserving of clemency. The White House has pointed back to those remarks every time the question has been raised since. Trump has pardoned several high-profile figures in the crypto space, including Silk Road founder Ross Ulbricht and former Binance CEO Changpeng Zhao, but Bankman-Fried occupies a different category. He was one of the largest donors to Joe Biden's 2020 presidential campaign, a fact that has not been forgotten, and the scale of the fraud, an estimated USD$8 billion (AU$11.4 billion) in customer funds, left real victims with real losses that have not been made whole.

The audacity of the filing is worth acknowledging without losing sight of what it represents. Bankman-Fried has spent the past year publicly echoing Trump's positions, granting a jailhouse interview to Tucker Carlson, and praising Trump's pardons of other controversial figures. The campaign for clemency has been deliberate and visible. Whether it works is almost beside the point. The more instructive question is what it says about an industry that is still working out how to hold its own history accountable while simultaneously asking regulators and politicians to trust it with the future.

The Bitcoin Analyst Who Still Sees USD$200,000

It is worth pausing, in the middle of two consecutive weeks of red, to note that not everyone has revised their outlook. A top Bitcoin analyst this week maintained a USD$200,000 (AU$284,940.80) price target, arguing that the current sell-off does not change the structural case for Bitcoin's long-term trajectory. The reasoning is not complicated: the same macro forces that are creating short-term pain, rising rates, liquidity contraction, and capital rotating into AI and IPOs are temporary conditions layered on top of a fundamental shift in how institutions, governments, and ordinary investors relate to Bitcoin as an asset class.

The bull case from here rests on a few pillars that the current price action has not dismantled. ETF access has permanently changed the addressable market for Bitcoin. Regulatory clarity in the US, while slower than the industry would like, is advancing. The Clarity Act remains in play. Sovereign interest in Bitcoin as a reserve asset, once considered fringe, is now a topic of serious policy discussion in multiple countries. Bitwise's model, covered in last week's edition, puts fair value at USD$224,000 (AU$319,133.70) on a sovereign default hedge basis. None of those numbers is a guarantee. What they represent is a framework for thinking about Bitcoin that extends beyond the current inflation print.

For Australian holders sitting with unrealised losses right now, the honest framing is the same one it has been for the past fortnight. The short-term pain is real. The long-term thesis is intact for those who had one in the first place. The more useful question than where the price goes next is whether you understood what you owned before the market started testing that understanding. At Wayex, we think the best time to get clear on that question is before a sell-off, not during one.

Crypto's Next Act: Real Assets Over Speculation

Reza Bandi, CEO of Atlas Capital, made an argument this week that deserves more attention than it got amid the market noise. Speaking to FXStreet, Bandi said the crypto industry's next major growth phase will not be driven by speculative trading but by the tokenisation of real-world assets, bringing traditional financial instruments like property, credit, and funds onto blockchain infrastructure in a way that makes them more accessible, more efficient, and more resilient. It is a thesis that has been building for several years, but the conditions for it are maturing faster than most people expected.

The case Bandi makes rests on three things. Tokenization makes fund operations leaner by streamlining back-end processes and reducing costs. It expands access by allowing investors around the world to participate in regulated financial products they could not previously reach. And it reduces dependence on traditional financial infrastructure that is increasingly vulnerable to geopolitical disruption. That last point is more relevant than it sounds. Bandi argues that as global conflicts increasingly target critical infrastructure, including power grids and communications networks, having financial rails that are more distributed and more resilient is not just a nice idea; it is a practical necessity.

His view on Bitcoin is measured rather than dismissive. He credits it with creating the excitement, the speculation, and the funding that made broader blockchain innovation possible. His caution is about what comes next. The more pressing challenge facing global markets, in his view, is not building better trading mechanisms but addressing the vulnerabilities in the monetary system itself. Tokenised real-world assets are the bridge between where crypto is and where it needs to go to be taken seriously at the institutional level. That bridge is already being built. Ondo Finance, which we covered in a previous edition, is one of the most visible examples of what it looks like when someone actually constructs it rather than just describing it.

Claude Mythos and the DeFi Scare

Anthropic, the AI company behind the Claude family of models, moved this week to expand access to Claude Mythos, its most advanced frontier model, which had previously been available only to a small group of trusted organisations through a program called Project Glasswing. The crypto community's reaction was swift and, in places, dramatic. Some DeFi participants called it a potential doomsday for the internet. Others advised users to revoke all token approvals and spread funds across multiple wallets. The fear centred on the model's reported ability to find software vulnerabilities better than all but the most skilled human security researchers, and what that capability might mean in the hands of bad actors targeting smart contracts and DeFi protocols.

The more measured voices in the room offered a useful correction. Curve Finance founder Michael Egorov argued that the model's ability to detect bugs in browser environments does not translate directly to smart contract exploits. The more realistic near-term risks, in his view, are operational security vulnerabilities: compromised multisig keys, supply chain attacks on frontend dependencies, and similar vectors that are serious but manageable for protocols with mature security practices. Anthropic's own researchers acknowledged the model's capabilities in a report on so-called N-day exploits, publicly disclosed vulnerabilities that can now be reverse-engineered into working attacks far faster than traditional patching cycles allow. Their conclusion was not that this is unmanageable but that the patching playbook the industry has relied on needs to change.

The honest take is somewhere between the panic and the dismissal. Claude Mythos is a genuinely capable model, and its expanded availability will create new attack surfaces that did not exist before. The protocols and custodians that have invested seriously in security infrastructure are better placed to absorb that than those that have not. For everyday crypto users, the practical advice is the same as it has always been: use platforms with robust compliance and security frameworks, be selective about which protocols you interact with, and treat anything that asks for broad wallet permissions with appropriate scepticism. The age of AI-assisted security cuts both ways. The defenders get the same tools as the attackers.

Founder's Corner

Two weeks of red markets have a way of sharpening your thinking. When prices are falling and the news cycle is full of conflict-of-interest investigations, pardon applications, and AI models that apparently spell doom for the internet, it is easy to lose the thread of why any of this matters in the first place.

The story that stayed with me this week was not the price action. It was the Reuters investigation into the Trump family's crypto ventures. Not because of the politics, but because of what it illustrates about a pattern that has repeated itself throughout this industry's history: when the incentives of the people promoting something are not aligned with the people buying it, someone always pays the price. The numbers in that investigation are not allegations. They are public record. And the lesson is not that crypto is uniquely corrupt. It is that crypto, like every other financial market, rewards people who read the fine print and penalises those who do not.

The RWA piece from Atlas Capital points in the direction I think this industry is actually heading. Not speculation, not meme coins, not politically connected token launches. Boring, useful, regulated infrastructure that gives more people access to more financial products with more transparency than the system they are replacing. That is a harder story to tell than a price chart going up. It is also the only version of this industry that survives long enough to matter.

At Wayex, that is the version we are building for. Regulated, compliant, and here for the long game.

Richard Voice, Co-Founder, Wayex

Something That Made Us Laugh This Week!