The market is in fear mode this week, and the numbers are real. Bitcoin has fallen to around US$63,000 (AU$88,360), down roughly 10% on the week; Strategy shares have shed more than 15% in five days, and altcoins are getting hit harder. The question worth sitting with is not whether the pain is real, it clearly is, but whether the story the market is telling itself about why is actually accurate. The honest read from some of the sharper analysts this week is that Bitcoin is not crashing because of Saylor; it is losing the momentum trade to AI stocks and IPOs. That is a very different problem, with a very different set of implications. Before the red charts make your decisions for you, let's get into what is actually happening.

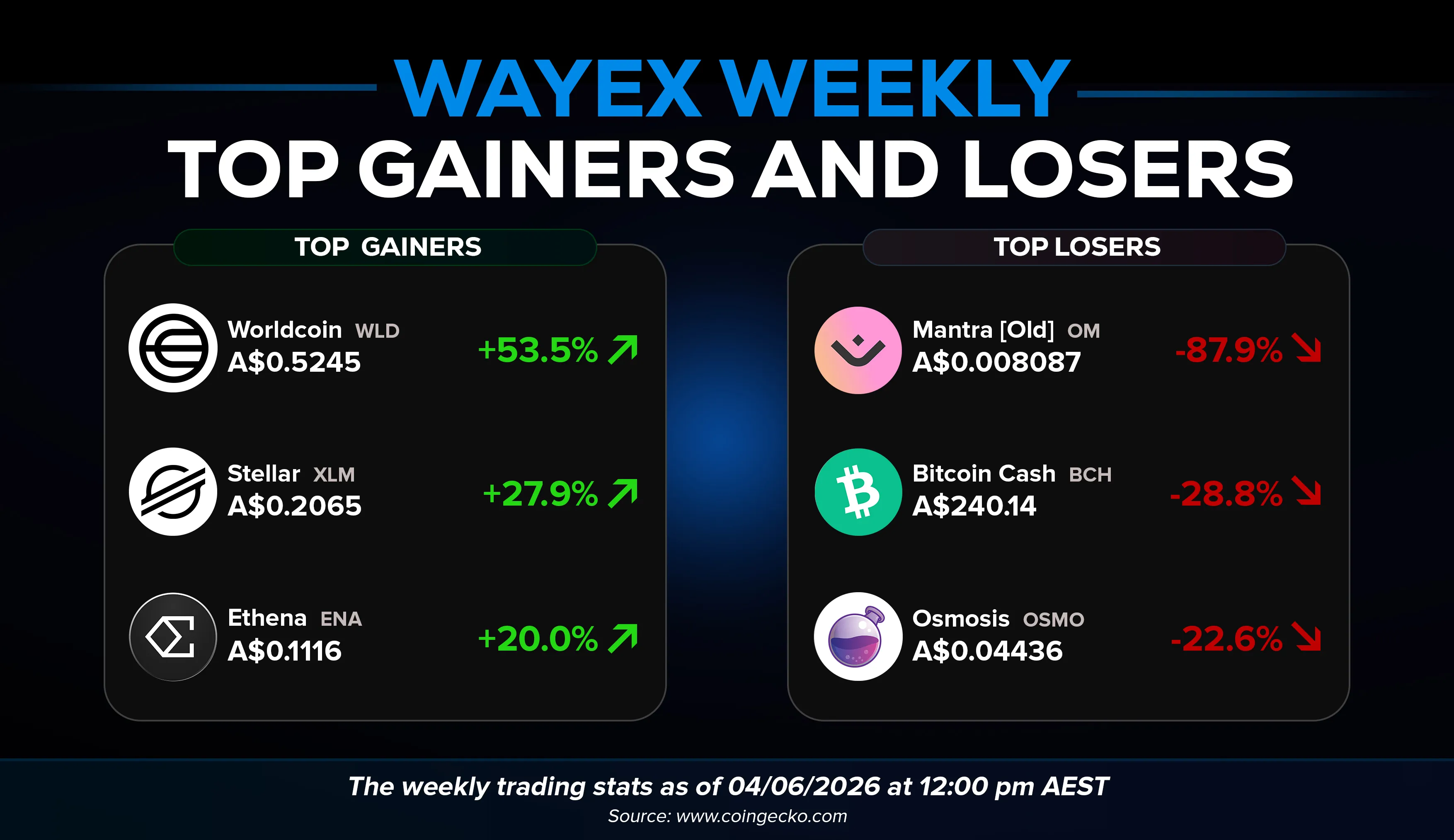

Top Gainers & Losers on Wayex

Is This a Crash or Just a Momentum Problem?

The dominant narrative this week has been that Michael Saylor broke the market. Strategy sold 32 BTC, shares dropped more than 9% in a single session and are now more than 70% off their 52-week high, and the crypto community did what it always does: looked for a villain. The more considered read, offered by Charles Schwab's director of digital currencies research, Jim Ferraioli, is less dramatic and more instructive. Bitcoin has been in a bear market since October. The recent weakness is not about fading institutional demand or Saylor's small BTC sale. It is about Bitcoin losing its status as the market's dominant momentum trade.

The mechanics are worth understanding. Crypto investors historically chase momentum, and right now, momentum is elsewhere. Capital that once flowed into BTC is rotating into AI-related equities, anticipated IPOs like OpenAI and SpaceX, and increasingly into non-crypto assets that can now be traded on crypto-native platforms like Hyperliquid. Bitcoin is no longer competing against other cryptocurrencies for speculative attention. It is competing against every major growth narrative in the market simultaneously, and summer seasonality, historically Bitcoin's weakest period, is not helping.

None of that makes the current price action comfortable to sit through. What it does mean is that the structural case for Bitcoin has not changed. ETF approvals, regulatory progress, and institutional adoption are all still intact. The Clarity Act remains in play in Washington. Bitwise has a model putting Bitcoin's fair value at US$224,000 (AU$314,247) as a sovereign default hedge. The market does not care about any of that right now because it is chasing something else. For long-term holders, the question is not whether the momentum trade has left. It is whether you believe it comes back. It has before.

When Institutions Bleed: Strategy and Bitmine

Strategy's rough week was not just a stock price story. The firm sold 32 BTC, a fraction of its more than US$56 billion (AU$79 billion) portfolio, and the market reacted as though a founding principle had been violated. Saylor had built his entire identity around never selling, and even a tiny, pre-telegraphed sale was enough to rattle confidence. The shares closed one session at US$136 (AU$190.76), down nearly 23% on the month and more than 70% off their 52-week high. TD Cowen analysts held their US$400 (AU$561.43) price target, a near 200% gain from current levels, but that kind of conviction is harder to hold when the chart looks like this.

The more striking institutional story of the week belongs to Bitmine. Tom Lee's Ethereum treasury firm has accumulated more than 5.3 million ETH and now sits on an estimated US$9 billion (AU$12.62 billion) unrealised loss as ETH has fallen below US$1,800 (AU$2,524.88). To raise fresh capital, the company announced a US$300 million (AU$420.81 million) preferred stock offering carrying a 9.5% annual dividend, borrowing directly from the Strategy playbook. The preferred shares will list on the NYSE under the ticker BMNP.

The timing is uncomfortable. Strategy's own preferred stock STRC fell below its US$100 par value this week as investors questioned whether dividend payments are sustainable while Bitcoin prices slide. Bitmine is launching a similar structure into the same headwind. The corporate crypto treasury model was built for a rising market. What this week tested is how it holds up when the market does the opposite. The answer is still being written, but the early chapters are not easy reading.

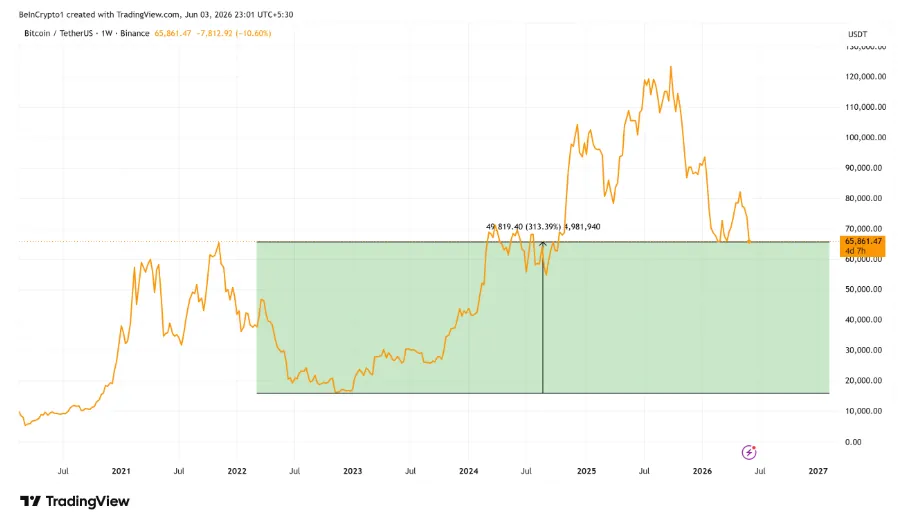

The One Chart That Changes the Conversation

When markets are in fear, the most valuable thing you can do is zoom out. Raoul Pal did exactly that this week, sharing a chart that has been making the rounds for good reason. Pal is the founder of Real Vision, a macro research and media platform, and a former Goldman Sachs hedge fund manager who has become one of the most-followed macro voices in the crypto space. The data shows Bitcoin significantly outperforming the Nasdaq on a global liquidity-adjusted basis over any meaningful time horizon.

The chart does not predict what happens next week or next month. What it does is reframe the question every long-term holder should be asking right now, which is not whether Bitcoin is down, it clearly is, but whether the underlying reason you hold it has changed. For most people who have thought carefully about why they own Bitcoin, the answer this week is no.

The liquidity argument matters because it is the most durable long-term case for Bitcoin that exists. Global liquidity cycles drive risk asset performance, and Bitcoin has historically been one of the most sensitive and responsive assets to those cycles. When liquidity expands, Bitcoin tends to amplify the move. When it contracts, as it has been doing, Bitcoin feels the pressure first and hardest. Ray Dalio made a related point this week from a different angle, warning that the AI bubble will not burst because the technology fails, but because investors will eventually need to convert paper wealth into cash to service debt, pay taxes, or meet redemptions. That liquidity squeeze, if it comes, hits every risk asset. Bitcoin included.

The honest framing for Australian crypto holders sitting with unrealised losses right now is this: the chart Raoul Pal shared is not a reason to ignore short-term pain. It is a reason to be clear about your time horizon before the market makes that decision for you. Wayex exists to give you a platform where you can act on that clarity when you are ready, not when you are panicking.

Cardano at a Crossroads

Charles Hoskinson warned this week that more Cardano projects could fail following the shutdown of TapTools, a widely used analytics platform that cited rising operating costs and unsustainable economics after four years of building on the network. Hoskinson said he had expected a wave of failures at the start of the year and that difficult market conditions, shrinking revenues, and limited access to capital had made it increasingly hard for ecosystem teams to keep operating. ADA is currently trading near US$0.20 (AU$0.28), down roughly 70% over the past year and more than 93% below its 2021 all-time high of US$3.09 (AU$4.33).

What makes the Cardano story more complicated than a simple bear market casualty is the funding debate sitting underneath it. Hoskinson pointed to a pattern of community resistance to treasury spending that could have supported ecosystem growth, including a failed vote to fund the annual Cardano Summit. He argues that the network has the technical foundation and the community to compete, but that the economic conditions are making it harder for businesses to survive long enough to prove it. The tension between a founder who wants to act and a decentralised community that wants to deliberate is not new to Cardano, but it is sharper now that projects are actually closing.

For ADA holders, the honest question is whether this is a network going through a painful but survivable correction or something more structural. The technical picture is mixed, the funding debate is unresolved, and Hoskinson himself has acknowledged that more project failures could follow. What is clear is that the outcome of the ecosystem's current governance tensions will matter more for Cardano's long-term trajectory than any single week of price action.

HYPE Defies the Market

While almost everything else in crypto was posting double-digit losses this week, Hyperliquid's HYPE token hit an all-time high of US$75.40 (AU$105,77) and briefly overtook Solana in price for the first time. SOL has fallen nearly 14% over the past month and slipped to its lowest level since late 2023, while HYPE has gained approximately 24% over the same period. The price crossover is symbolic rather than structural. Solana's market capitalisation of over US$41 billion (AU$57.52 billion) still dwarfs Hyperliquid's US$16.5 billion (AU$23.15 billion), but the momentum story it represents is real and worth paying attention to.

Hyperliquid is a decentralised perpetuals exchange, and the numbers behind its growth are not hype. The platform captured a record 6.63% share of global perpetual futures trading volume in May, with its builder-deployed contracts generating more than US$62 billion (AU$86.9 billion) in monthly trading activity. Institutional products are following the user activity. Grayscale launched its HYPG Hyperliquid Staking ETF this week, joining earlier products from 21Shares and Bitwise that have already attracted more than US$136 million (AU$190.79 million) in net inflows within their first three weeks.

The HYPE story connects directly to the momentum rotation we covered earlier in this edition. Charles Schwab's Jim Ferraioli noted this week that crypto-native platforms like Hyperliquid are now allowing traders to speculate on private company shares, commodities, and other non-crypto assets via perpetual contracts. Bitcoin is losing momentum partly because platforms like Hyperliquid are capturing it. That is not a reason to dismiss Bitcoin. It is a reason to understand that the competitive landscape for speculative capital inside crypto is changing faster than most people expected, and that new winners are emerging in real time.

Ray Dalio's Warning and the Quantum Paradox

Two stories this week that did not fit neatly into the fear narrative but deserve attention from anyone thinking about crypto beyond the next price candle. The first is Ray Dalio's warning about the AI bubble, delivered in a Bloomberg television interview. Dalio, the founder of Bridgewater Associates and one of the most respected macro investors alive, is not predicting that AI fails as a technology. His argument is more specific and more unsettling: the bubble bursts when investors need to convert paper wealth into cash. Debt payments, wealth taxes, and fund redemptions can each trigger forced selling at scale. Bridgewater estimates that Alphabet, Amazon, Meta, and Microsoft alone could invest around US$650 billion (AU$911.85 billion) in AI infrastructure during 2026. That is a lot of paper wealth sitting in a system that runs on actual money. When the squeeze comes, it will reach every risk asset, and crypto will not be exempt.

The second story is more counterintuitive and worth sitting with. A report from Swiss custody firm Taurus this week turned the standard quantum computing doomsday narrative on its head. The conventional fear is that a sufficiently powerful quantum computer could break Bitcoin's encryption and allow an attacker to steal funds. The Taurus analysis points out the flaw in that logic: a quantum attack capable of breaking Bitcoin would trigger an immediate market collapse before any theft could settle on-chain. The attacker would destroy the value of the prize before collecting it. The real quantum risk, the report argues, is not Bitcoin theft but the harvesting of confidential encrypted data today for decryption later, a threat that sits well outside most retail investors' concerns. Post-quantum cryptography is not a reason to panic. It is a reason for custodians and institutions to act, and the serious ones already are.

Founder's Corner

Fear weeks are useful. Not because they are comfortable, but because they show a different side to just positive trends. When prices are rising, everyone is a long-term believer. When they are falling, you find out pretty quickly what people actually think they own and why they own it.

The honest read on this week is that the market is not broken. It is rotating. Capital is chasing AI stocks, anticipated IPOs, and new platforms that did not exist two years ago. Bitcoin is feeling the competition in real time. That is a different problem from the ones that caused previous crypto winters, and it is worth being precise about the difference. The fundamentals that matter, regulatory progress, institutional adoption, ETF access, have not deteriorated. The momentum trade has moved elsewhere for now. It has done that before.

What I keep coming back to is the Raoul Pal chart. On a liquidity-adjusted basis, Bitcoin has outperformed the Nasdaq over any meaningful time horizon. That does not make this week's losses easier to look at. What it does is remind you that the question worth asking right now is not what the price is doing. It is whether your reason for being here has changed. For most people who have thought carefully about that question, the answer is no.

At Wayex, we built a regulated, compliant platform for exactly these moments. Not to tell you what to do with your portfolio, but to make sure that when you are ready to act with clarity rather than panic, the platform is there and the rails are sound.

Richard Voice, Co-Founder, Wayex

Something That Made Us Laugh This Week!