This week in crypto feels like the market finally stopped pretending everything was fine. Bitcoin dropped below US$77,000 (AU$107,416.35) as geopolitical tensions, inflation fears, and higher US Treasury yields weighed on risk assets, and the data beneath the price tells a more uncomfortable story than most people want to sit with. Spot Bitcoin ETFs shed another US$648.64 (AU$913.29) million in a single day, following last week's US$1 billion (AU$1.4 billion) in outflows, as BlackRock's IBIT led the exit with US$448 million (AU$630.79 million) in redemptions alone. That is not noise. That is institutional money making a deliberate decision about risk. Michael Burry, the investor who called the 2008 housing crash, issued a fresh warning this week, this time targeting the convergence of crypto and traditional equities, calling the direction of travel a harbinger of a cyberpunk future that needs to be stopped. Meanwhile, an expert warned publicly that even a mountain of T-bills might not protect Tether and Circle from a sudden liquidity crisis. Trump signed an executive order pushing crypto firms closer to the Fed's payment rails, which is genuinely positive news, but it landed in a week where the cautionary signals were too loud to ignore. The infrastructure story remains intact. The short-term environment is asking harder questions than usual.

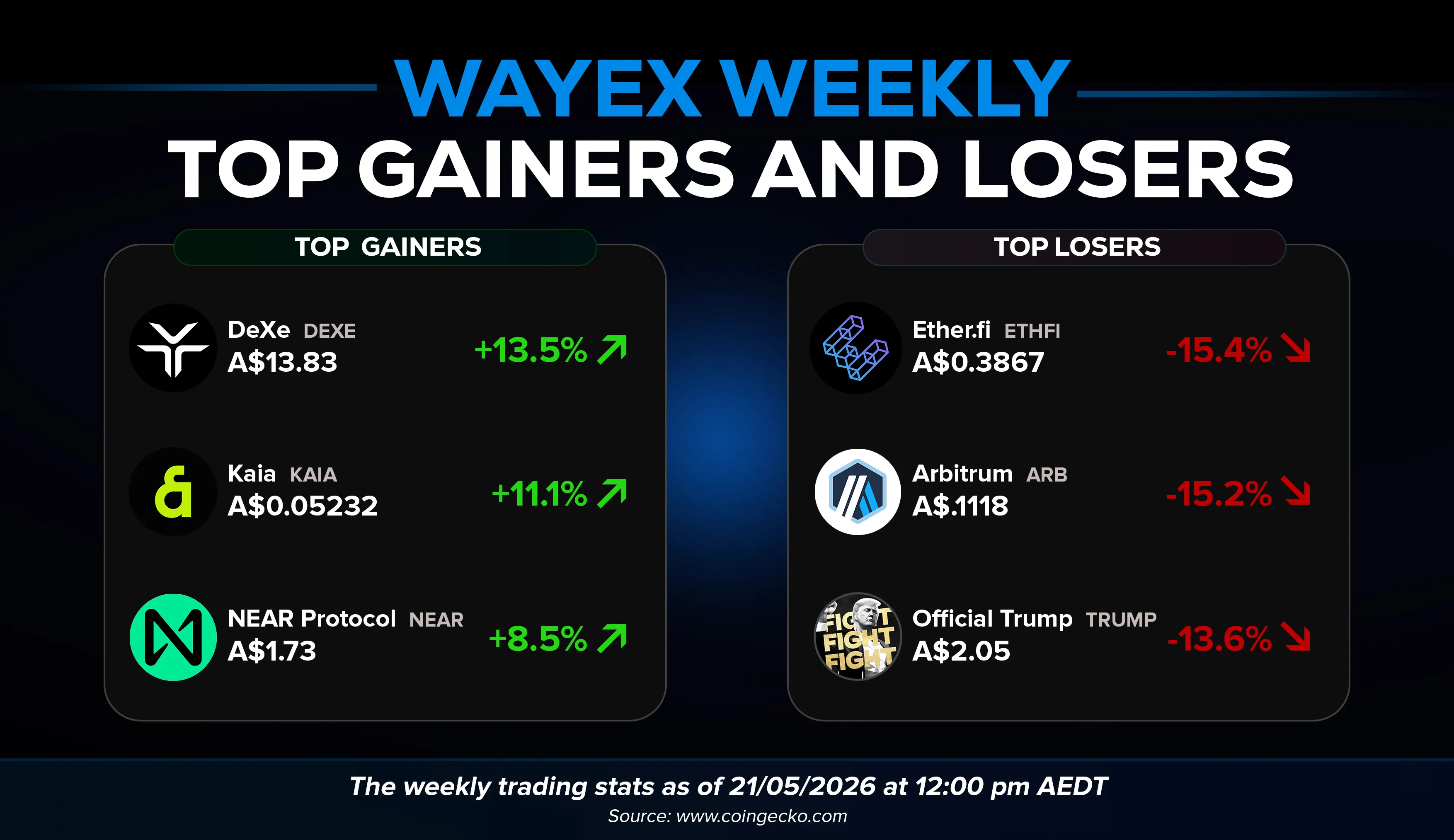

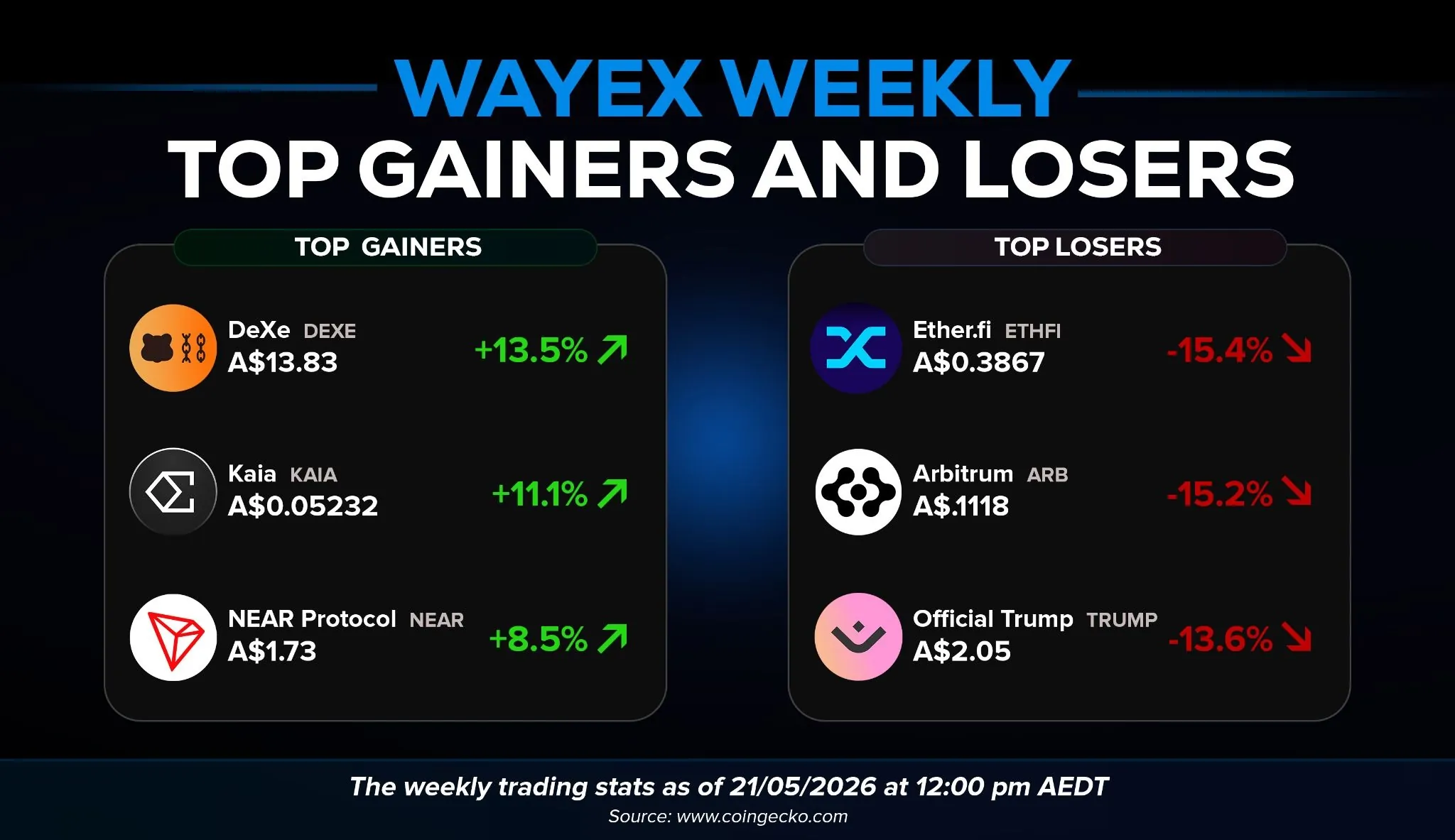

Top Gainers & Losers on Wayex

Market sentiment? Currently “Neutral”.

Trump, The Fed, and Crypto's Access to Payment Rails

President Trump signed an executive order on May 19 directing federal financial regulators, including the Federal Reserve, to review rules and practices that limit fintech and digital asset firms' access to US payment systems, with findings due within 90 days. On the surface, this is straightforwardly good news for crypto. The US payment system, including the Federal Reserve's FedNow and wire transfer services, has largely been off-limits to crypto-native firms. Many digital asset companies have struggled to secure banking partnerships, forcing them to rely on a small number of crypto-friendly banks or operate without direct access to the central banking system.

The order requires agencies to examine rules, guidance, supervisory practices, and application processes that affect nonbank companies using technology to offer or support financial products and services. Covered activities include payment processing, lending, digital banking, securities and commodities market activity, blockchain-based services and other digital asset services. In practical terms, this could open the door for stablecoin issuers, digital asset exchanges, and blockchain-based payment processors to obtain direct access to the rails that the traditional financial system runs on.

The context matters, though. This executive order arrives at a moment when Trump is simultaneously pressuring the newly confirmed Kevin Warsh to cut rates in an inflationary environment, and the relationship between the White House and the Fed has never been more politically charged. The Federal Reserve Bank of Kansas has already granted Kraken, a Wyoming special-purpose depository institution, access to a limited version of its master account. Ripple, Anchorage Digital, and fintech money transfer company Wise also hope to win master accounts. The direction is right. Whether an administration with this much political heat behind it can execute cleanly on something this technically complex is the open question. For platforms like Wayex operating in regulated markets, the principle of crypto firms gaining proper payment rail access is one we have been building toward. The path to get there is going to be complicated.

Fund Managers Are Derisking, And The Numbers Show It

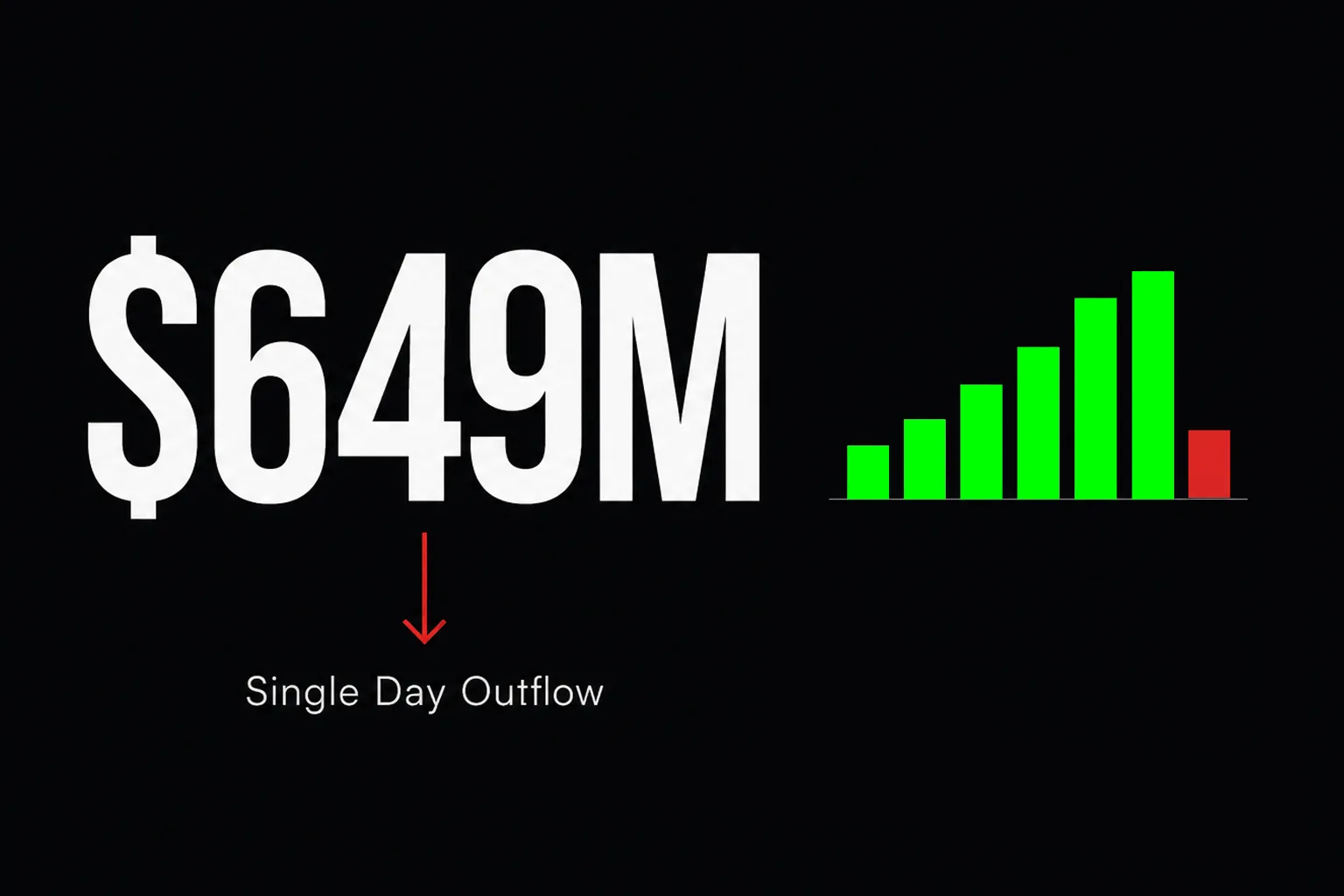

Spot Bitcoin ETFs recorded their largest single-day net outflows since January 29, with US$648.64 million (AU$913.29 million) in net outflows across seven funds on Monday, extending last week's total net outflows of US$1 billion (AU$1.4 billion), which ended a six-week positive streak. This is the kind of data point that deserves more than a passing mention. Six weeks of consistent inflows represented real institutional conviction. One week of reversals at this scale represents something equally real going the other way.

The outflows are correlated to the general market and reflect the derisking strategy conducted by fund managers in light of geopolitical events, amid the recent escalation in the US-Iran conflict. The outflows were also driven by last week's US inflation data, which significantly shifted market expectations around Federal Reserve policy, with rising expectations of a rate hike this year. Those two forces pulling in the same direction at the same time are not a coincidence. When geopolitical risk pushes oil prices higher, energy-driven inflation follows, and the case for rate cuts evaporates. When rate cuts evaporate, the tailwind that has been supporting risk assets like Bitcoin disappears with them. CoinDesk

US-listed spot Bitcoin ETFs have seen over US$1.5 billion (AU$2.1 billion) in outflows since May 7, signalling sustained institutional selling pressure. Trading metrics show aggressive selling in both spot and futures markets and rising demand for protective put options, indicating growing concern about a deeper price decline. The honest read on this is not panic, but it is not comfort either. Institutions are not abandoning Bitcoin as a long-term asset class. They are managing short-term risk in an environment that is asking them to be careful. The difference between those two things matters enormously for how you interpret what happens next. Long-term holders have been accumulating through this weakness, which historically limits how far the downside goes. That is the counterweight worth holding onto right now.

Michael Burry Is Paying Attention. You Should Too.

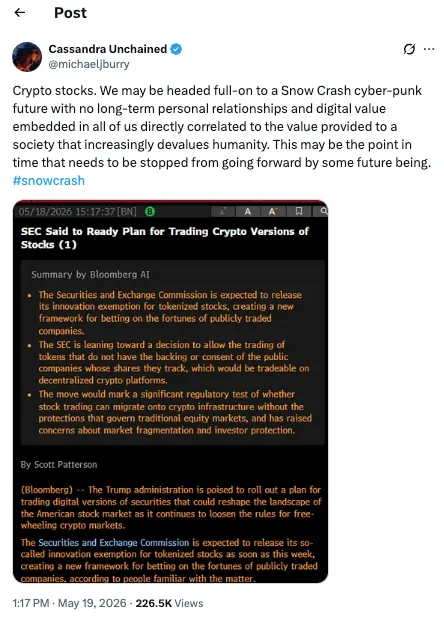

Michael Burry, the investor who famously predicted the 2008 housing crash, issued a warning this week targeting the convergence of crypto and traditional equities, calling tokenised stocks a harbinger of a slide into a Snow Crash cyberpunk future and describing the moment as one that needs to be stopped. Burry does not post often, and he does not post casually. When he raises his hand, it is worth understanding what he is actually saying rather than dismissing it or catastrophising it.

His concern this week was specifically directed at the SEC's reported move toward an innovation exemption that would allow tokenised stocks to trade on crypto platforms without the company's permission, and potentially without voting rights or dividends attached. For Burry, this is not just a regulatory footnote. It is a structural warning about the direction financial markets are heading, where the lines between real assets and digital representations of those assets blur in ways that create systemic risks most participants do not fully understand yet.

Bitcoin has spent much of 2026 trading like a high-risk tech asset, with its correlation to the Nasdaq hitting a record 0.96 in April, meaning a Nasdaq selloff could drag crypto down with it, regardless of its digital gold narrative. That is the part of Burry's broader thesis that matters most for crypto holders right now. If he is right that the AI-driven Nasdaq rally mirrors the final frenzied months of the dot-com bubble, and if Bitcoin continues to move in lockstep with tech stocks, then a significant equity correction does not leave crypto standing as a safe haven. It takes crypto down with it.

Research shows the correlation is asymmetric as Bitcoin tends to follow Nasdaq selloffs closely, but sometimes ignores equity rallies entirely. For investors, that is the worst of both worlds: limited upside sharing, but full downside exposure when tech corrects. Burry is not telling anyone to sell. He is raising his hand and pointing at a structural vulnerability that deserves serious thought. In a week where fund managers are already pulling US$649 million (AU$914.08 million) out of Bitcoin ETFs in a single day, his timing is not something to scroll past.

Why The Clarity Act Still Matters, Maybe More Than Ever

The Clarity Act cleared the Senate Banking Committee on May 14 and is now heading toward a full Senate floor vote. Given everything happening in the macro environment this week, it would be easy to treat this as background noise. It is anything but. The Clarity Act is the single most important piece of legislation the crypto industry has ever had this close to becoming law, and the chaotic macro backdrop of this week is precisely why it matters more, not less.

The bill establishes clear rules separating which digital assets are securities and which are commodities, ending the jurisdictional confusion between the SEC and CFTC that has plagued the industry for years. It protects software developers who publish code without controlling customer funds. It preserves the right to self-custody. It requires digital asset exchanges, brokers, and dealers to comply with Bank Secrecy Act regulations, including anti-money laundering programs, suspicious activity reporting, and sanctions compliance. In short, it gives the industry the structural certainty it needs to attract the kind of serious, long-term institutional capital that does not get spooked by a week of ETF outflows.

The remaining hurdle is the conflict-of-interest provision, with Democrats insisting the bill cannot pass the Senate floor without language restricting government officials from profiting from the crypto industry. The bill still needs 60 votes to clear the Senate, which requires bipartisan support. That is not a small ask in the current political environment. What makes this week's cautionary signals relevant to the Clarity Act story is the direct connection between regulatory uncertainty and institutional risk management. The US$649 million (AU$914.08 million) in ETF outflows, the Burry warnings, and the stablecoin vulnerability concerns we cover below are all of these are symptoms of an industry that has grown large enough to attract serious capital but has not yet secured the regulatory foundation that serious capital ultimately requires. The Clarity Act is that foundation. The July 4 target date the White House set remains in play. Watch this space closely.

USDT and USDC: Is The Stablecoin Safety Net Thinner Than We Think?

This is the story of the week that deserves the most careful reading, and possibly the least amount of panic. An expert warned publicly this week that even a mountain of Treasury bills will not save Tether and Circle from a sudden liquidity crisis, and the argument being made is more technically grounded than the headline suggests. It is worth understanding properly rather than either dismissing it or spiralling into alarm.

The core argument is structural. Both Tether and Circle hold the majority of their reserves in short-term US Treasury bills, which are widely considered among the safest assets on earth. The problem is not the quality of the assets. The problem is the speed at which a redemption crisis can unfold. In a sudden confidence shock, where a large number of holders simultaneously demand redemption, the time it takes to liquidate even high-quality assets like T-bills, settle the trades, and return fiat to users can create a gap between the demand for liquidity and the ability to supply it. That gap, even if temporary, can trigger the kind of bank-run dynamic that turns a manageable situation into a systemic one.

This matters particularly this week because stablecoins sit at the intersection of almost every other story in this newsletter. They are central to how crypto firms would use Fed payment rails if Trump's executive order leads anywhere. They are the assets institutional investors hold when they derisk out of Bitcoin ETFs. They are the settlement layer for tokenised equities and real-world assets. The Clarity Act includes specific provisions around stablecoin regulation that were contested enough to nearly derail the entire bill. The expert warning this week is not a prediction that Tether or Circle will fail. It is a reminder that size and safety are not the same thing, and that as stablecoins become more systemically important, the consequences of a liquidity event become more systemically dangerous. Good record keeping, understanding what you hold and why, and using regulated platforms matter more than ever. Your Wayex account holds your full transaction history. That clarity is worth having.

The Infrastructure Keeps Building: HYPE and Tokenised Equities

After five sections of cautionary signals, here is the part of the week worth holding onto. Two stories this week pointed to the same underlying truth: regardless of what the macro environment is doing in the short term, the infrastructure being built on top of blockchain rails keeps compounding. This is the long game, and this week it made meaningful progress on two fronts.

Bitwise, one of the more credible institutional voices in the crypto asset management space, called HYPE a generation-two crypto token this week and flagged it as undervalued. The distinction between generation-one and generation-two tokens matters more than it might sound. Generation-one tokens are primarily stores of value or speculative assets. Generation-two tokens have actual utility built into functioning ecosystems with real revenue, real users, and real network effects. Bitwise making that call publicly about HYPE is a signal worth paying attention to, not because it constitutes investment advice, but because it reflects a broader shift in how serious institutional analysts are thinking about what gives a crypto asset durable value beyond the cycle.

The tokenised equities story is even more significant, and this is where Michael Burry's warning from section 3 meets its counterargument. The SEC is reportedly preparing to launch an innovation exemption for tokenised stocks, possibly as soon as this week, which would allow trading of tokens that track a company's stock price on decentralised crypto venues. The market has already voted with its capital. Tokenised equities hit an all-time high of US$3.57 billion (AU$5.03 billion) in daily volume this week, a number that would have seemed implausible two years ago. Burry's concern about where this leads structurally is legitimate and worth taking seriously. The volume data tells you that the market is moving in this direction regardless. The infrastructure is not waiting for everyone to agree it is a good idea before it gets built. The question for participants is not whether tokenised equities become a meaningful part of financial markets; that question is already being answered. The question is whether the regulatory framework catches up fast enough to make it safe.

Founder’s Corner

This week in crypto feels like the market finally stopped pretending everything was fine. Bitcoin dropped below US$77,000 (AU$108,416.35) as geopolitical tensions, inflation fears, and higher US Treasury yields weighed on risk assets, and the data beneath the price tells a more uncomfortable story than most people want to sit with.

Spot Bitcoin ETFs shed US$648.64 million (AU$913.29 million) in a single day, following last week's US$1 billion (AU$1.4 billion) in outflows, with BlackRock's IBIT leading the exit with US$448 million (AU$630.98 million) in redemptions alone. That is not noise. That is institutional money making a deliberate decision about risk. Michael Burry, the investor who called the 2008 housing crash, issued a fresh warning this week targeting the convergence of crypto and traditional equities, calling the direction of travel a harbinger of a cyberpunk future that needs to be stopped.

Meanwhile, an expert warned publicly that even a mountain of T-bills might not protect Tether and Circle from a sudden liquidity crisis. Trump signed an executive order pushing crypto firms closer to the Fed's payment rails, which is genuinely positive news, and something that we are already on top of with Wayex Global. However, it landed in a week where the cautionary signals were too loud to ignore. The infrastructure story remains intact. The short-term environment is asking harder questions than usual.

Things That Made Us Laugh This Week